The ECB published a Working Paper this month, with the interesting title On secular stagnation and low interest rate: demography matters. As we are used from the ECB, it is a thorough piece of research, especially helpful if you want to get a bit of an update on the latest ideas on the subject. Having said that, there are a couple things that I find peculiar in this study.

First the methodology. “We conduct a backward-looking counterfactual scenario analysis” What is it with the ECB and counterfactual? Draghi seems to be using the word quite regularly (here, here and here) and the ECB somehow prefers it as a way to present their results in their studies (as in here and here). Is it just me who has an ‘alternative facts’ association with the word counterfactual? But it gets worse: “In addition, we present a forward-looking counterfactual assessment.” Huh? Don’t you need a factional (the future, that is) to start talking about a counterfactual anymore? This is too much overkill if you ask me. By definition, the counterfactual cannot be known, not in the past, but certainly not in the future. Call me an old grump, but it is called a projection, people, not a forward-looking counterfactual assessment…

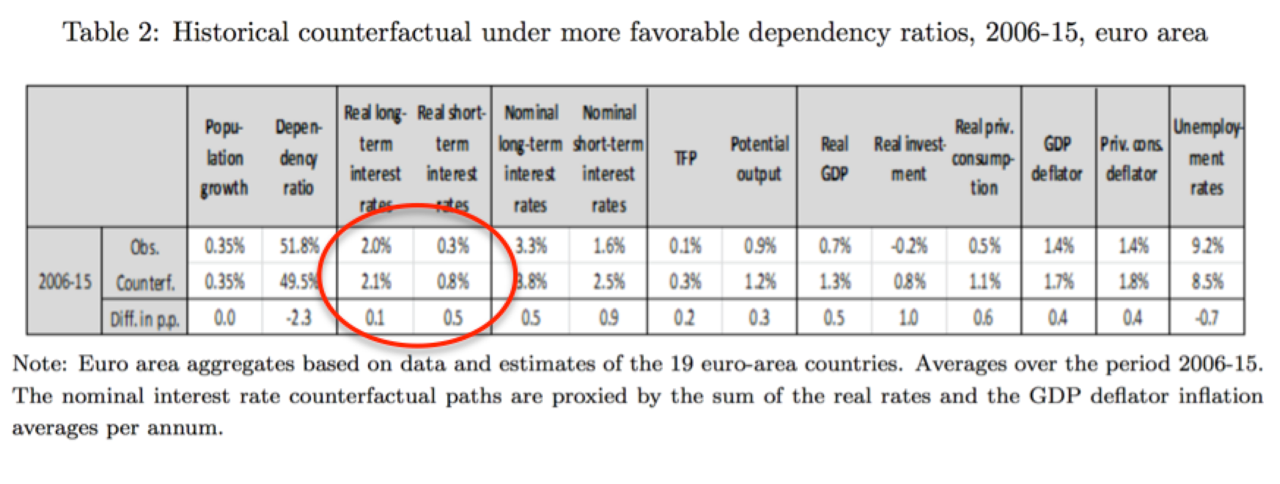

Then the results. I quote from the abstract: “The main conclusion that we draw from our empirical, panel equation system-based assessment is that these developments have exerted downward pressures on real short- and long-term interest rates in the euro area over the past decade.” (emphasises are mine) Sounds logical. We all save to retire, more savings push rates and bond yields down. Here is the table with the results:

Talk about underwhelming. Real bond yields have been 2.0% and would have been 2.1% in the counterfactual world. 10bps! So, the bond market reaction following Draghi’s speech at Sintra was (bond yields rose by +13 bps) was bigger than the whole impact of effect of ageing combined? I think I would have formulated my conclusion somewhat different, in that case. Something like: “There has been virtually no impact on real bond yields” (which I find hard to believe, actually, but hey, let’s not argue with the facts).

To defend the researchers: there has been an impact on real short rates: from the factual 0.3% to the counterfactual (that we cannot know) of 0.8%. This sounds substantial enough to warrant the “downward pressures on real short- and long-term interest rates” bit, but this does raise the question what has been the cause behind this drop: ageing people or policy choices by the council of the ECB? On the one hand one can claim that the ECB reacts to what happens in the world, but on the other there is a fair amount of discretion of the policy chosen. As an example, the Federal Reserve never lowered interest rate below 0%, whereas the ECB pushed its deposit rate to -0.4%.

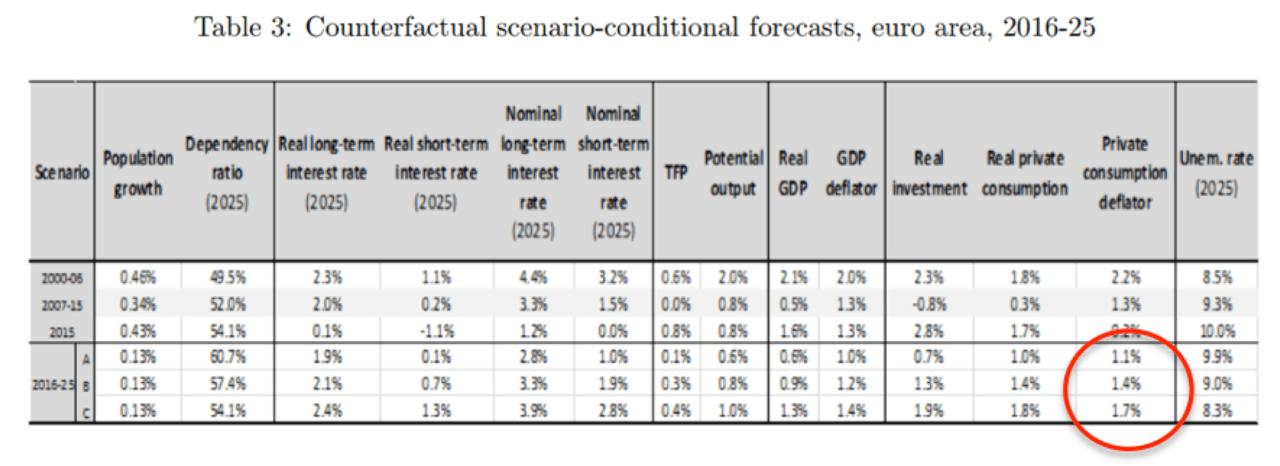

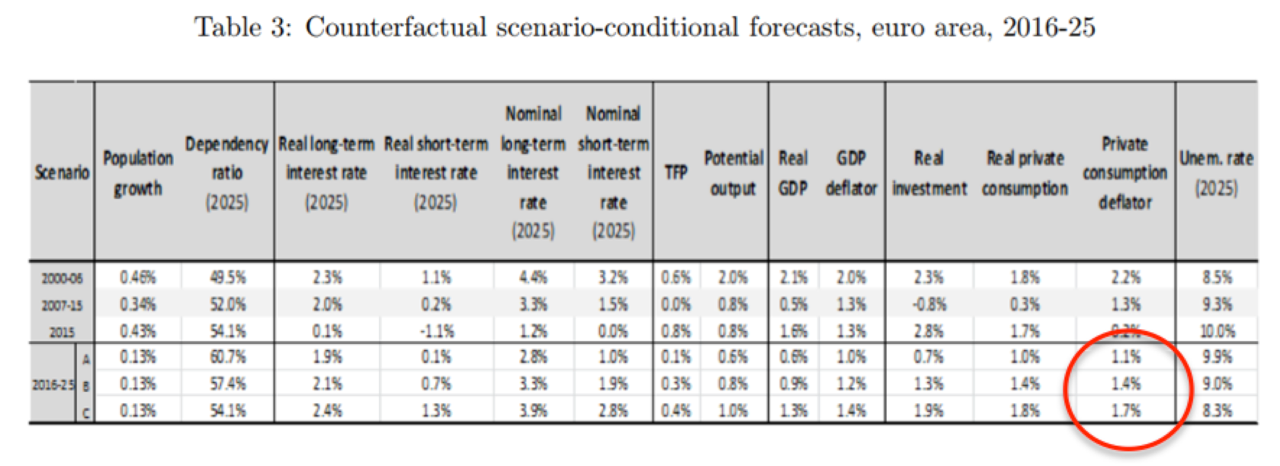

So why boast this downward pressure on bond yields and interest rates as much, by putting it centre stage in the title? Maybe the answer can be found by looking at the forward-looking counterfactual assessment projection:

Three scenarios are being presented for the future, all with different dependency ratios. The interesting part of this table is the projection of the private consumer deflator: even in the best outcome scenario (dependency rates remaining stable from the 2015 level) inflation will on average reach 1.7%: in the two more realistic scenarios inflation will average 1.4% and 1.1% respectively. In other words, according to this piece of research, the ECB will not be able to reach its inflation target the next ten years. Counterfactually so!

Somehow, I can see why that has not made it to the title of the Working Paper…

Ze zijn vaak goed, maar dit is een pareltje 😉

Cheers!

Pingback: Best of the Web: 17-08-02 nr 1717 | Best of the Web

Pingback: Morning News: August 2, 2017 – Paydee