http://www.crossingwallstreet.com/archives/2017/07/near-to-high-point-of-the-election-cycle.html

You probably missed the press release, but it’s official: don’t expect anything from equities over the coming 14 months.

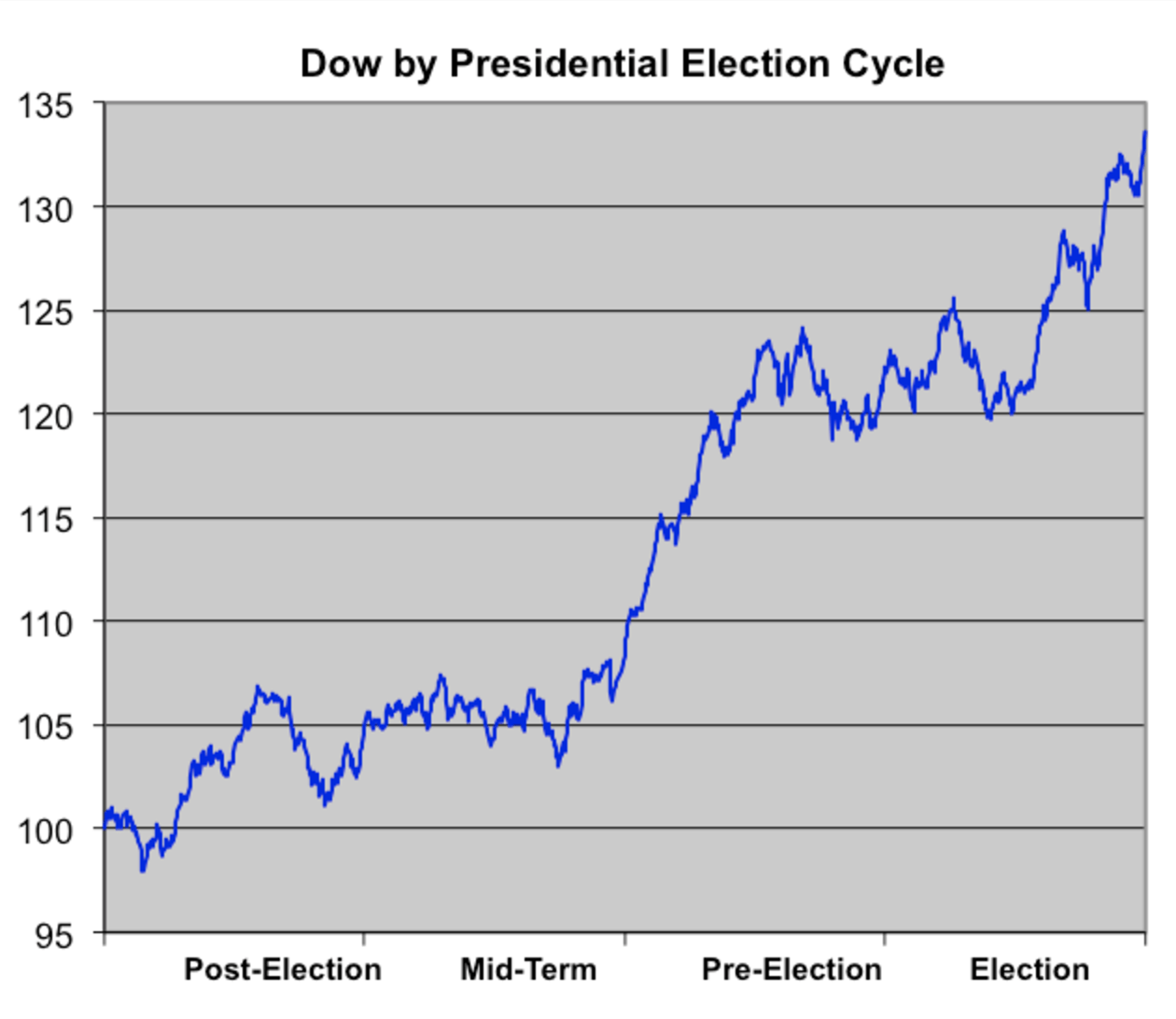

Time for a vacation! And not for just a couple of weeks. No, best just go away until September next year. At least that’s my generous interpretation of this week’s graph. I’ll be honest though, the prospects of my own pending vacation might have clouded my judgement on this.

So what does this graph tell us? The line shows the historic development of the Dow Jones over the four years of a US presidency. Specifically, it relates to the average course of the 30 presidential cycles that have occurred over the last 120 years. So we’re not talking about the last 30 presidents: otherwise we’d have to go all the way back to Franklin Pierce, who bore the scepter in the period 1853-57. The graph ignores re-elections, impeachments or deaths: every four years, the clock resets and gives us an average, resulting in the graph above.

As it turns out, in historical terms returns are generated in only two of the four years. The first up-trend occurs in the election year and runs until the end of July of the President’s first year in office. The markets then go flat, only pursuing the upward line again around September of the President’s second year in office. The so-called midterm elections (the elections for the House of Representatives and part of the Senate) in November then often signal the beginning of a very strong rally, subsequently leading to another period of flat markets.

Presidential cycle

What we see here is known as the Presidential Cycle, a phenomenon we’ve been aware of since 1967. The popular explanation for this pattern is found in the ups and downs that the president faces during his term of office. Initially you have the positive momentum of a new government/president, that will result in the promised change of course. But enthusiasm cools off once it turns out that these promises are not all being kept, or once it becomes clear that the changes might also involve painful side effects. Once the new Congress is installed (midterms), workable compromises are found and the positive momentum returns. Or something along those lines, at least, though we’ve never seen convincing proof that markets are that strongly influenced by politics. In that sense, the Presidential Cycle belongs in the set of strange anomalies, like Sell in May, or the turn of the month effect. They seem to exist, but why they exist is not always clear.

The risk of such a line is that it is often quite convincing. An alternative rendering looks as follows:

The last two years in particular seem strong

Source: Robeco, Bloomberg

In this graph, I have used the data from the last 88 years, and I am considering the S&P500, so there is definitely some noise compared to the data in the first graph. In this graph, I have divided the 21 cycles into four blocks of twenty years, giving us some idea as to what degree this is a stable phenomenon. The black line shows the average development over the entire period.

What strikes me is that the result appears to be reasonably stable and reliable for the third (and fourth) year, but that there is actually a great deal of variation in the first two years. So going on vacation based on one simple line seems a little too naive. But if you’re still not convinced, then I’ve got another graph for you:

In practice, the cycle is a little less predictable…

Source: Robeco, Bloomberg

Here too, we see the average development (green line), as well as all 21 cycles completed since 1928: you can clearly see that the average actually says little when you look at each individual cycle. The black line in this graph shows the development of the S&P500 since Trump’s victory. While the average president would be looking at price gains of 5% at this point, Trump has already managed to generate a 14% profit. Given that the sense of disappointment might play a modest role, you’d expect the rejection of the Obamacare repeal to have put some kind of dent in market sentiment. But nothing is further from the truth: the S&P500 hit a new all-time high earlier this week.

A strong start could of course mean that the flat period lasts much longer, perhaps? That’s definitely a possibility, but it’s not what has happened in the past. In the following graph, I’ve only left in the lines showing markets reacting at least as enthusiastically as they did to Trump’s win. The 1932-36 cycle is a doubtful case: heavy losses in the first few weeks reversed to become major gains by July. Including that cycle, there are eight terms of office in which the markets were stronger at the end of July than Trump’s 14%. The green line shows the average development of these eight cycles. Until May of the second year, gains rose fairly uniformly, turning somewhat thereafter. The average gain of these ‘strong starters’ over the entire four years (50%!) is much higher than the average for all terms.

Strong starters are strong finishers. Mostly…

Source: Robeco, Bloomberg

So it’s time to go long Trump? Past performance is no guarantee of future results, and that most certainly applies to the Presidential Cycle. That we cannot talk here of a law, is nicely demonstrated by the outlier in this last graph. It is the only ‘strong starter’ cycle that ended with a loss. And that’s not to mention one other, err, minor loss: in the 1928-1932 cycle, the S&P500 took a hit of no less than 80%…