Source: Bloomberg, Robeco

Given the number of camera crews traveling through the Netherlands last week, hoping to capture angry PVV voters’ interpretation of events, you might be forgiven for thinking that the Netherlands is a major player on the international stage, when it comes to elections. Certainly for Dutch politics and future policy, the results are of vital importance, but anyone who thinks the financial markets will take much notice is probably deluding themselves.

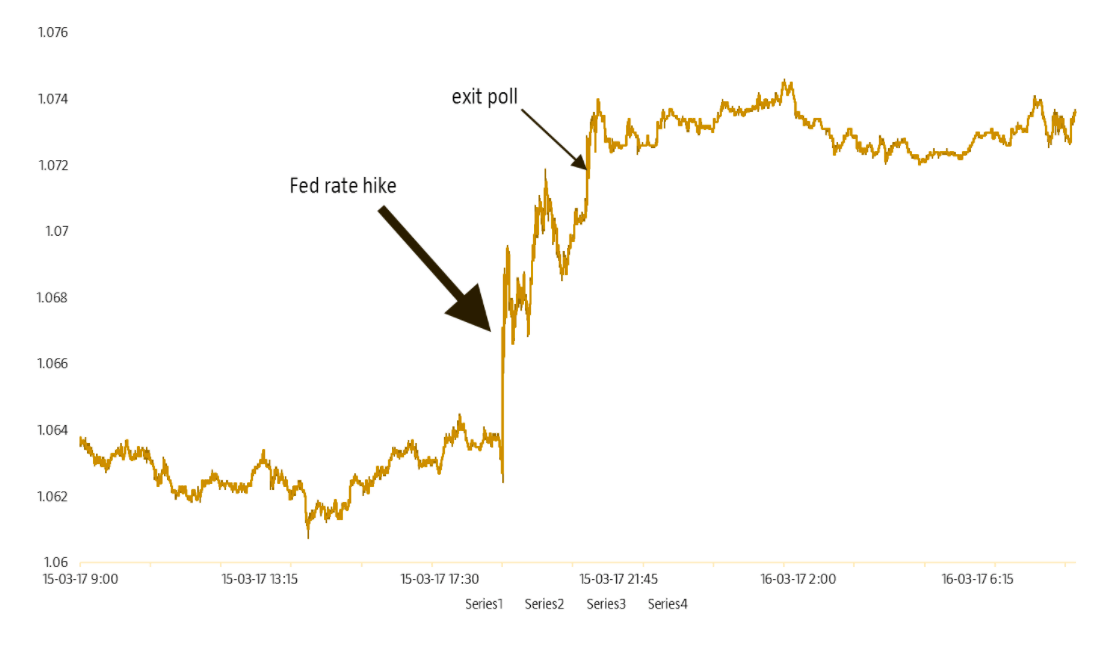

It’s not that they didn’t react at all. The currency markets responded positively at 9:00h on the back of the first exit poll, which showed that the PVV was not the biggest party. The euro appreciated by about 1.2 cents against the US dollar. However, if we look at the movement during the day, most of this gain turns out to be related to the Fed’s interest-rate decision, that was announced at 19:00h Dutch time. The gains associated with the Dutch election result amounted to 0.3 cents at most. Not exactly a result that would normally faze the markets.

Bonds couldn’t care less

The European bond market also seemed pretty relaxed that morning. The spread between the French and German yield narrowed temporarily by just four basis points. Four basis points is financial market nerd speak for 0.004 %. Is that a lot? The best way to answer that is with a graph of bond spreads relative to Germany, as shown below. It’s true that the last movement is down, but if I reproduce this graph again in two months time and ask you to show me when the election was, I don’t think you’ll be able to do it. It’s more of a case of incidental noise than a really strong change in sentiment. Dutch yields only gave up two basis points relative to Germany: nothing to really get excited about.

French bond market benefits from election result

Source: Bloomberg

Stocks? *yawn*

What about stocks? That’s debatable too. It’s easy to establish that the European markets rose the day after the election, but whether this is related to the election outcome or is the result of a higher close in the US, is open to interpretation. At any rate it is certainly not as if the Dutch market performed significantly better on 16 March than the other European markets: we were somewhere in the middle. So this post-election picture does not really differ much from what has happened after previous Dutch elections. The graph below shows the frequency distribution of the differences between the Dutch market and the broader European market. The breakdown is normal: the Netherlands performs about as well or badly as the broader European market, but the daily differences can be quite significant. However the greater the differences are, the less frequently they occur. The arrows in the chart indicate the relative stock market movements on the day after the previous eight elections. This also confirms that Dutch elections are little more than noise and do not really have a significant impact on the financial markets.

So yes, if you really try hard you can see the effects of the Dutch elections on the financial markets. But you do need a magnifying glass to do it. In a historical context, last week’s election certainly had no major impact on the markets and so, in that respect, it did not really differ from past elections. Of course this in no way changes how important the elections are for the Netherlands themselves: I, for one, am happy that, to cite Prime Minister Mark Rutte, ‘the wrong kind of populism did not win’.

Although it does make me wonder what the ‘right kind of populism’ might be…