Ever since Trump’s election, there have been grave concerns that the US will crack down on countries with large trade surpluses. But are they justified?

Among Trump’s many promises on the campaign trail, ending what he considers unfair trade practices was one of his spearheads. He not only called the North American Trade Agreement (NAFTA), “the worst trade deal in history”, but also promised to pull out of the Trans Pacific Partnership (TPP) on his first day in office and pledged to bring jobs that were lost to China back to the US. But how? For one thing, by putting pressure on the companies themselves. For example, he said that from now on, Apple should produce iPhones in the US, car maker Ford should withdraw its investments in a Mexican factory and that he won’t eat any more Oreo cookies until Nabisco moves production back the US. And he didn’t stop at the companies ─ he also plans to put pressure on countries in order to make America great again. Among his other verbal assaults, which were mainly aimed at Mexico and China, Trump stated that labeling China a currency manipulator would be one of the new Treasury Secretary’s first orders of business.

As a what? A currency manipulator. According to an act passed in 1988, the US Department of the Treasury is authorized to challenge foreign exchange policies that place the US at an unfair disadvantage. In that case, the US can enter negotiations to challenge the policies, which in the first few years, did in fact happen. Taiwan, Korea and China were accused of being manipulators. In negotiations with the US, they were then placed under pressure and changed their policies as a result. But since then, not much has happened, because after 1994, the Treasury couldn’t identify any new cases of currency manipulation ─ much to the chagrin of a few Republican senators, who have been lobbying since 2003 to have China labeled a manipulator. Remarkably, it didn’t matter whether a Republican (Bush) or Democrat (Obama) was in office ─ no one proved willing to pull the political trigger. What the US had intended to use as a weapon to defend itself against the rest of the world, quickly became an obligation for the Treasury Department, which bent over backwards each year to avoid finding cases of manipulation at all costs.

Three criteria

The Senate’s relentless criticism has since been addressed by issuing an official definition, consisting of three criteria which must be met before a country may be called a currency manipulator, namely:

- The country must have run a trade surplus with the US of more than USD 20 billion for a period of 12 months.

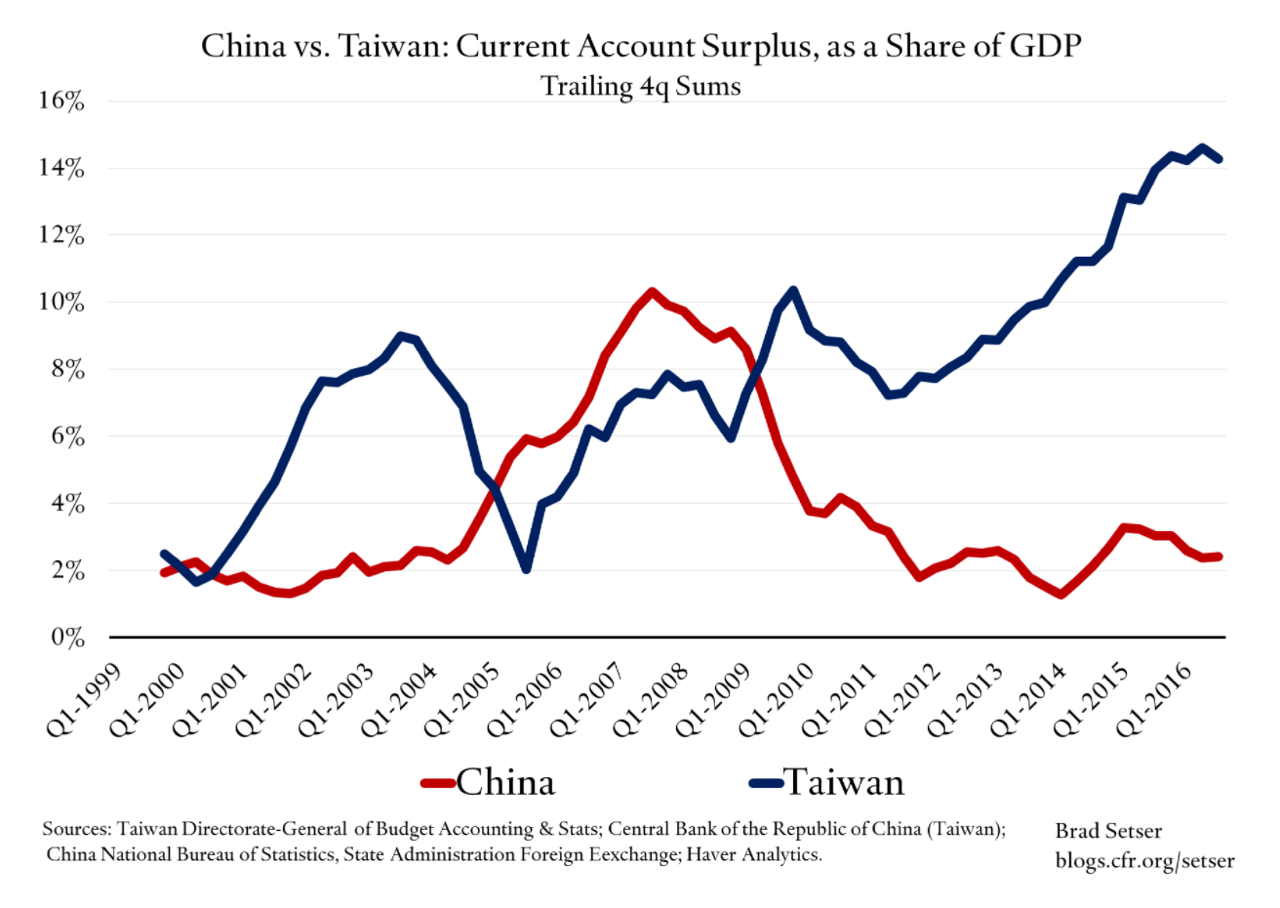

- It must have a large current account surplus (over 3% of GDP)

-

It buys foreign currency on a large scale in order to depreciate its own (more than 2% of GDP in the last 12 months)

This last point may need some explaining. Normally, a country with a large current account surplus will receive more and more foreign currency. For the sake of simplicity, let’s say it’s dollars. And you can’t buy much in Germany with dollars, so these will probably be exchanged for euros, putting downward pressure on the dollar. This has a corrective effect: the currencies of countries with high current account surpluses become stronger, making them less competitive abroad, which in turn lowers the current account surplus. Central banks can counteract this process by buying foreign currency.

With all this in mind, we can work out which countries are now in the danger zone. First, in terms of their trade surplus with the US (or, equivalently, the US trade deficit with the countries involved). There are currently three countries that have well exceeded the USD 20 billion ceiling, and one which is borderline. Of those three, China is the biggest outlier, exceeding the limit by a factor of ten (USD 350 billion), while the figures for Germany and Japan are just under USD 70 billion. Korea is on the cusp with USD 28 billion, while Taiwan is at number five with a surplus of USD 14 billion. In case you were wondering about Mexico, it doesn’t have a trade surplus with the US at all, but a marginal deficit, in fact…

Changes in trade balance over time

Source: Bloomberg, Robeco

And the current account surpluses of these suspects are shown here:

Many countries have consistently had current account surplus

Source: IMF, Robeco

Four of the five countries already mentioned also meet the second criterion. Taiwan is the clear outlier, with a current account surplus of as much as 15% of GDP. Germany is a close second, and China is notable by its absence: according the IMF’s data, its current account surplus amounts to only 2.4% of GDP. As such, so far only three countries have met the first two criteria: Germany, Japan and Korea. So what about Mexico? Mexico has a current account deficit of 2.7%…

This brings us to the last, and most complex point: foreign currency purchases. I don’t have a nice graph for that one, but this criterion appears to only be met by one of the five countries: Taiwan. Though it’s not clear whether its purchases exceed 2% of GDP. As for Korea and China, in recent quarters, both have actually been selling foreign currency, which in fact supports their own currencies. Neither Germany (=ECB), nor Japan have intervened.

In short, based on the existing rules, no one is at risk of being called a currency manipulator. In fact, even if a country were branded such, the direct consequences appear to be limited: after all, when the US became a member of the World Trade Organization (WTO) in 1994, it accepted that trade conflicts would be resolved within the framework of the WTO. Unilaterally imposing tariffs on China, for instance, would clearly go against WTO regulations and could only be done after years of negotiation.

Sigh of relief?

So can we all breathe a sigh of relief? Unfortunately, it’s not quite that simple, either. According to the current rules, the US has only fairly limited room for maneuver, but who says Trump will play by the rules? He could still pull out of NAFTA on the day he takes office (after which the agreement would expire within six months). During his campaign, he also made it clear he wanted to invoke laws that applied before the WTO existed. On that basis, President Bush placed an import tariff on steel in 2002, which apparently did not violate WTO regulations, either. And so a general import levy seems unlikely, but by targeting certain key sectors, Trump can still push his agenda, without calling anyone a manipulator. But then again, I don’t think the Treasury’s rules have much bearing on Trump’s choice of words, so I won’t be at all surprised if he uses the term manipulator at some point…