http://uk.businessinsider.com/us-consumer-only-thing-not-in-recession-2016-8

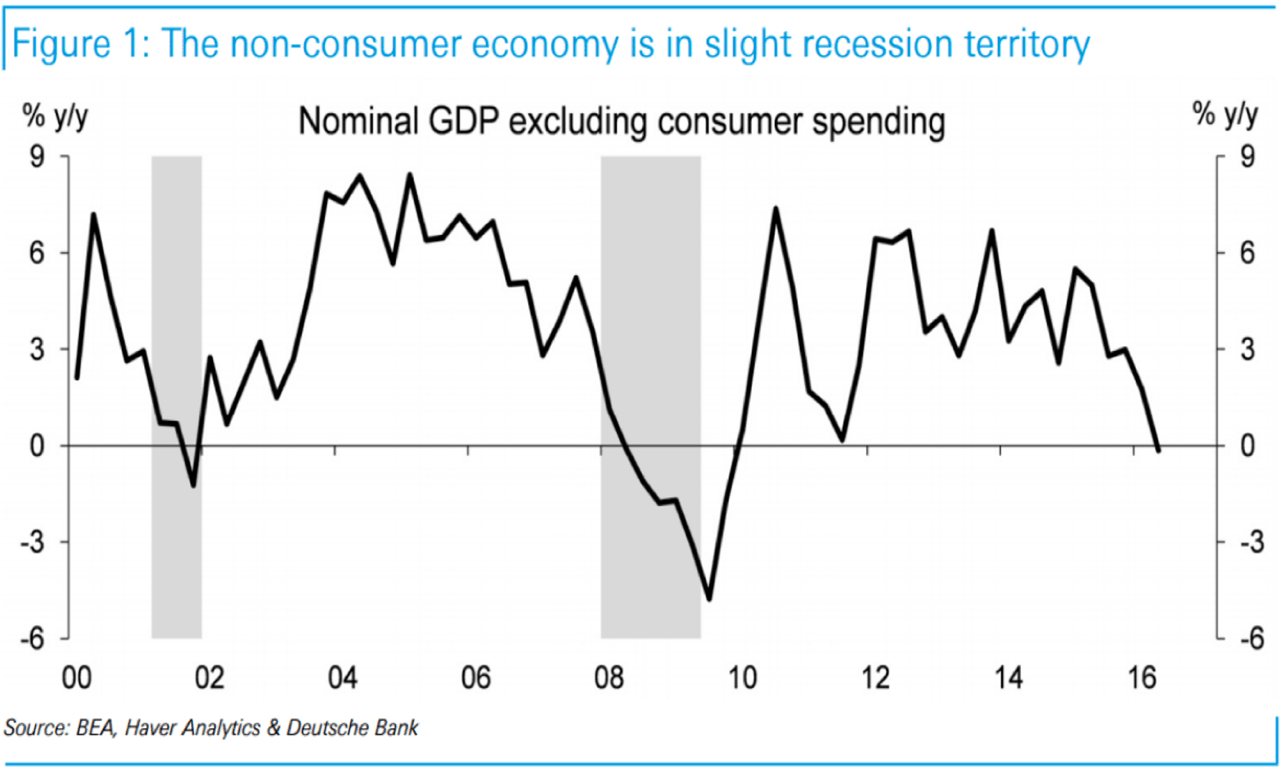

I haven’t seen one for a while, but I stumbled across another one just this week: a graph that shows the US is closer to recession than we think…

Graphs with just one line are usually simple affairs, and today’s graph of the week is no exception. The line shows the growth pattern, and the gray areas are the periods in which the US economy was officially in recession. Indeed, the decline at the end of the period doesn’t look very encouraging and appears to suggest that the US economy is about to enter a recession: growth has dived into negative territory.

Negative? But wasn’t there a GDP report released last week that shows that the US economy had grown 1.2% in the second quarter? Disappointing growth, sure, but still positive: so where did that slight contraction suddenly come from? The answer is quite simple: the graph is not showing the development of the entire GDP, but just a part of it. Specifically, we’re looking at the growth of all spending components, excluding consumption. Investments, government spending, the external sector: chuck it all on one pile and then calculate growth. The idea behind this is to show how dependent the US economy actually is on just a single component of spending: the consumer. So the ominous message is: what if consumers also now throw in the towel…

Initially I thought this was an interesting idea. It sheds light on a different aspect of the economy, one that is weaker than you might have previously expected. However, the more I thought about it, the more I concluded that this graph is not really much use to man or beast.

What if?

Let’s start with the ‘what if’ approach: what if the US consumer now throws in the towel? If you understand that the weight of the US consumer counts for some 70% of total GDP, you would very rapidly come to the conclusion that this is a pretty stupid question. If the US consumer throws in the towel, the US is in recession: simple. If 70% of GDP contracts, we’d need a small miracle if the other 30% were to compensate. However, miracles like that never happen: companies are not usually too keen on investing when consumers are spending less. If we add consumption and investments together, then we end up with a weight of 85% of GDP. The growth of the other 15% is really not going to offset that.

And if you don’t believe me: the graph below shows the development of real GDP (black line), consumption (turquoise line) and the rest (orange line). And indeed: on no occasion has the turquoise line gone negative without a recession having been entered. Conversely, the graph also clearly shows that it is very possible for the other components (orange line) to show a decline without this leading to recession.

Source: Robeco & Bloomberg

Now the sharper reader will have noticed that the orange line is quite a bit more negative than the black line in the first graph. And that brings us to our second objection to the first graph: why did they choose to look at nominal data? Since recessions are always determined on the basis of real data, it would be far more logical to look at that. I thought I’d just take a look at the real data.

Source: Robeco & Bloomberg

The black line in this graph corresponds with the black line from the first graph and shows the nominal value. The orange line on the other hand gives us the development of the real value. Unsurprisingly, the orange line is often lower, but the difference has become considerably less in recent years (with the disappearance of inflation). So what’s the upshot? Well, looking at the black line, you get the feeling that a decline below zero is pretty much unique and only really happens in recessionary periods. However, if you look at the orange line, you’ll see that the zero point is frequently reached (zero growth), or even breached (contraction), not only during recessions, but also in the healthy expansion phase during the nineties. The cause is fairly simple: the strong deterioration in the US current-account deficit has often resulted in ‘the other 30%’ showing no growth. It should be obvious that this absolutely does not mean by definition that the economy is teetering on the verge of recession. Therefore, the black line (nominal) suggests a stronger causation than is actually the case.