http://www.coppolacomment.com/2016/05/the-safe-asset-scarcity-problem-2050.html

This week’s graph shoes the demise of high-quality government bonds, which suggests the end of risk-free investing. Or maybe not?

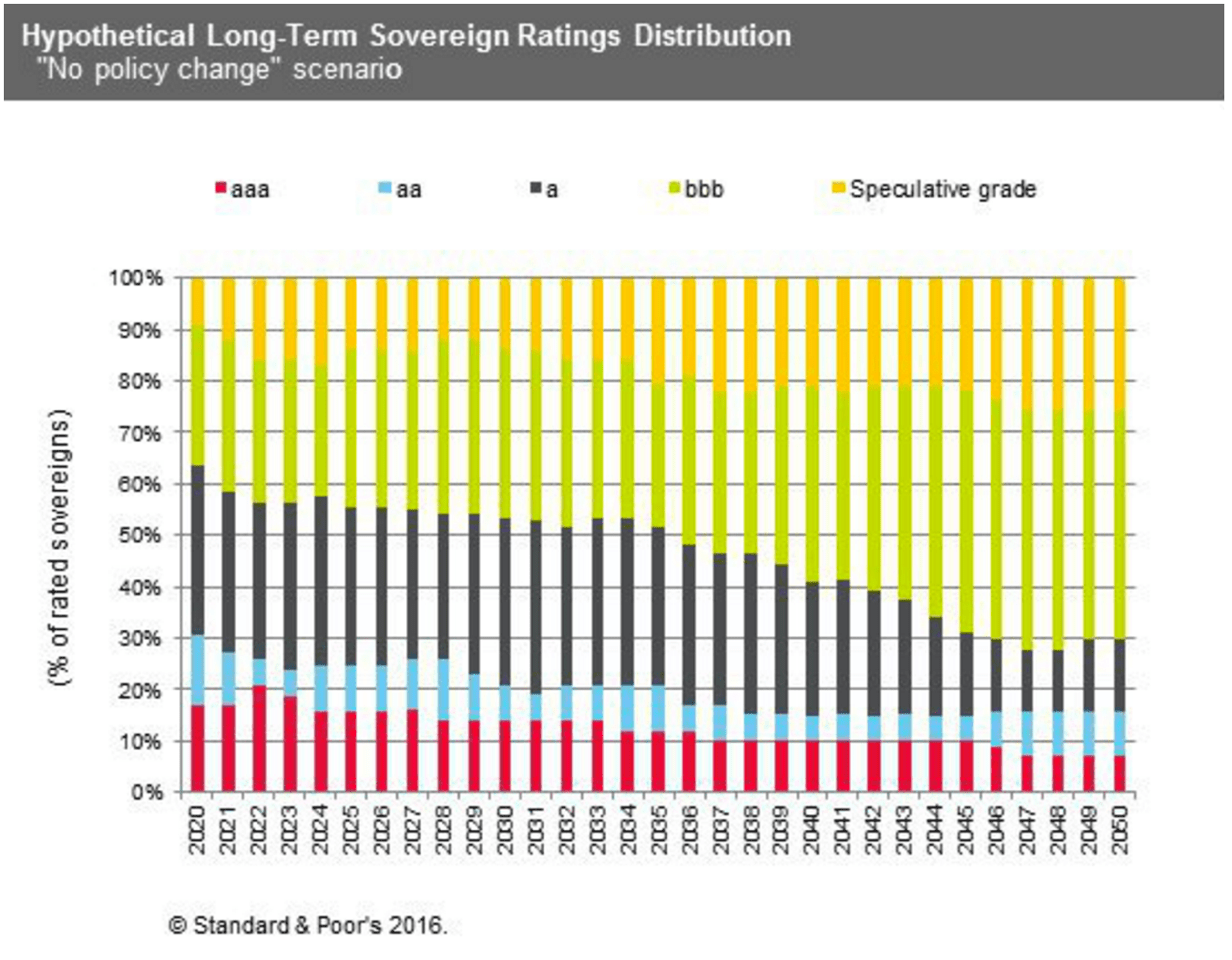

It’s a great graph, this one. Originating from credit rating company Standard & Poor’s, it shows a projection of the composition of the global market for government bonds for the period 2020 to 2050. It takes account of the creditworthiness of the different countries, running from the highest credit rating (AAA, in red) to the lowest rating (shown here as speculative grade, in yellow). For the record, Germany, the Netherlands and Switzerland are examples of countries with an AAA rating, America currently has to make do with an AA rating, Italy and Spain should be grateful with a BBB rating, while you have to go to countries like Nigeria, Turkey or Brazil to find the speculative grade segment.

The message appears to be pretty clear at first: high-quality government debt will come under pressure over the next thirty years, while the weaker segments on the other hand will improve. But beware, this is a shift that would take place in a ‘no policy change’ scenario, which seems to suggest that there is also an alternative scenario that would give a different picture. Unfortunately, I haven’t got the underlying report, but as far as I understand, it relates to an analysis of the costs of aging.

Now, you won’t hear me suggesting that aging isn’t a serious issue with potentially far-reaching consequences for the financial position of governments, but those that think that it signals the end of risk-free government bonds, has got the wrong end of the stick.

Crystal balls

To start with, I thought I remembered having seen this graph before. It took me a while, but thanks to my painstaking work of collecting graphs on a daily basis, I was able to find it on my website (www.lukasdaalder.com). This is a graph published by Standard & Poor’s in a 2010 report:

https://lukasdaalder.com/2010/10/11/best-links-of-the-web10-10-11-nr-184/

It won’t have escaped your attention that this graph has a more somber tone than the first one. In this second graph, government debt in 2050 will be made up of 60% speculative grade bonds, with the 2016 update sticking at 25%. But one thing can be stated with certainty: in this second graph, there’s little debate to be had about the demise of AAA bonds. By 2031, there won’t be any gilt-edged bonds left, although they make a minor (but mysterious) comeback in 2040.

And although in this case, too, I don’t have the underlying analysis, it shows that the outcome is quite sensitive to the basic assumptions. The 2010 graph clearly assumed a fairly negative scenario in terms of underlying growth and the related debt position. With all due respect to the analysis of Standard & Poor’s – I’m assuming that they have carried out thorough research – and prediction is of course always a hairy business, but it really does feel like this method allows you to show any outcome you want. After looking at the 2010 graph, I’m not really so impressed any more by the 2016 version.

But isn’t that always the case?

My second criticism is that although the graph does show its composition, it doesn’t cover the development of total debt. And that just happens to be the variable that changes everything. What’s more, in a scenario in which worldwide public debt rises faster than the size of the global economy, the pattern shown will basically arise by definition. After all, creditworthiness is an absolute benchmark and is not relative. However, that doesn’t have to mean at all that there will be fewer AAA bonds in future. I can easily picture a scenario in which the absolute size of outstanding AAA debt is gradually increasing, while the relative volume is actually decreasing. All you need is for the debt of countries with a lower creditworthiness to rise faster than that of countries with an AAA rating. To say that AAA bonds will become scarcer on the basis of this graph is entirely unsubstantiated.

But just how risk-free is risk-free?

Finally one general point: let’s not exaggerate the ‘risk-free’ character of those AAA bonds. The graph below shows the price development of German 10-year bonds from April last year. If you had bought gilt-edged bonds at the unfortunate moment of 20 April, you would have faced a loss of 8% over the next eight weeks. You could of course say that this was a temporary loss, given that we know these bonds return to their original value in the end (after 10 years), but what if you are forced to sell the bonds earlier?

Price development of German government bonds

Source: Bloomberg/Robeco