http://awealthofcommonsense.com/2016/03/how-much-do-profits-matter-to-stock-market-returns/

The idea that profit growth is a good indication of what kind of return you can generate on stock markets turns out to be too simplistic.

I’m not sure who said the following or even whether I’ve reproduced it correctly, but there is a saying that stock markets and economic growth are two drunkards connected to one another by a piece of elastic. In other words, economic growth can sway to the left, and stocks can stagger to the right, but eventually they drift so far from one another that the elastic starts to get really stretched. At that point, like a headstrong drunk, the market will try to stagger just a few paces further, only increasing the tension of the elastic more. But when the correction comes, the market not only flies back towards growth, but is unlikely to stop once having reached the level of growth: neither the elastic, nor the drunken state is any guarantee of balance. So stock markets sway to the left, and economic growth staggers to the right.

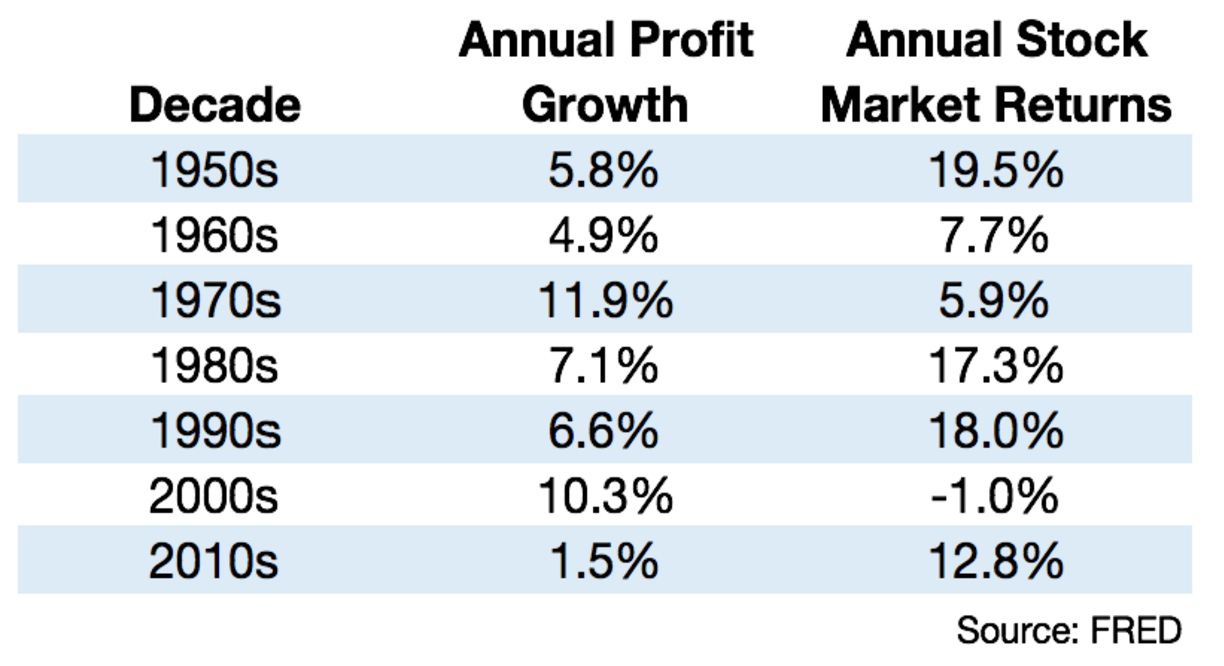

And that is basically what we see if we look at today’s table. I’ve touched on this subject once before, but at that point I was looking at the link between economic growth and stock markets: the table above very specifically shows profit growth and the market. You would expect a reasonably strong link, wouldn’t you? Equities perform well when corporate profits increase and perform less when profits disappoint. Seems logical.

And yet, as this table shows, such a link is barely perceptible. The left-hand column shows absolute profit growth of the US economy, divided into decades. The right-hand column gives the total returns that you would have generated with an investment in the US stock market, also per decade. The two drunkards with their piece of elastic are clearly visible. In the 80s and 90s, you would have generated an annual (!) return of around 18% with an investment in the S&P500, while the nominal corporate profit growth was ‘just’ 6.6%. Corporate profits then increased to 10% per year in the first ten years of the new century, but the market wasn’t interested: on balance you’d have lost 1% per year for ten whole years with your equity investment.

So no link, then? Err, yes, for sure: although that piece of elastic gives some room for movement, if you look over a long enough time period, this drunken staggering is evened out. Ten years is simply not a long enough horizon. What’s more, the decade-divide seems somewhat arbitrary. To show what I mean, I’ve tried to reproduce the table above, as a check that I am working with the same data. With mixed results, I have to say straight away, as while the stock-market returns are more or less correct, I haven’t managed to find the same series for profit growth. This might be down to a different underlying series (although I also used FRED), or due to different methods of calculation (should you take quarterly data, or rather yearly averages?), but whichever way you cut it, the numbers just don’t add up. However, this doesn’t change the underlying picture substantially, so I’ll just accept this margin of error for what it is.

If I then show the two underlying series in a graph, using logarithmic axes, this gives us the following picture.

Source: Bloomberg, Robeco

Your first reaction is probably that the graph clearly indicates that the market is far too optimistic. Whereas corporate profits have shown an average annual growth since 1947 of 7.4%, an equity investment in the S&P500 would have generated an average return of 11.1%. If the analogy of the elastic really is correct, that would mean there is a great deal of tension on the line.

However, the reaction is not correct. This graph compares profit growth with the total return on equities, and that’s like comparing apples and pears. If you look at how the total return on equities is structured, you’ll see that dividend plays an important role. Companies pay out part of their profits in the form of dividend and that is – to a certain degree – distinct from profit growth. Not distinct from profits, but from profit growth. This is simply illustrated by looking at an example of a company that manages to produce exactly the same profit every year, with half paid out in the form of dividend. There is no profit growth, and let’s assume that the share price also doesn’t change. In that case, the return for the shareholder is entirely made up of the (unchanged) dividend that is paid out every year. Zero profit growth, but still an annual return. Dividends are a bit like the coupon on bonds. Under normal circumstances, a company’s stock will therefore always generate a higher return over time than the growth in its profits.

It is thus more accurate to look not at the total return, but at the price gains of the equity investment (less dividend): if this consistently exceeds growth, then we can talk of our piece of elastic being stretched ever further. And that’s what the graph below shows us.

Source: Bloomberg, Robeco

So it turns out that, over this longer period, the two lines have shown similar growth. However, if you shorten the time period (as in the table above), you notice that the piece of elastic provides sufficient stretch to accommodate the inevitable deviations.

And one last point: that the black and turquoise lines have currently arrived at the same point seems to be encouraging, but doesn’t really tell us very much. The profit growth I use is profit growth for the entire US economy, while the stock market is just the largest 500 companies. And there’s clearly an elastic dynamic between those two series.