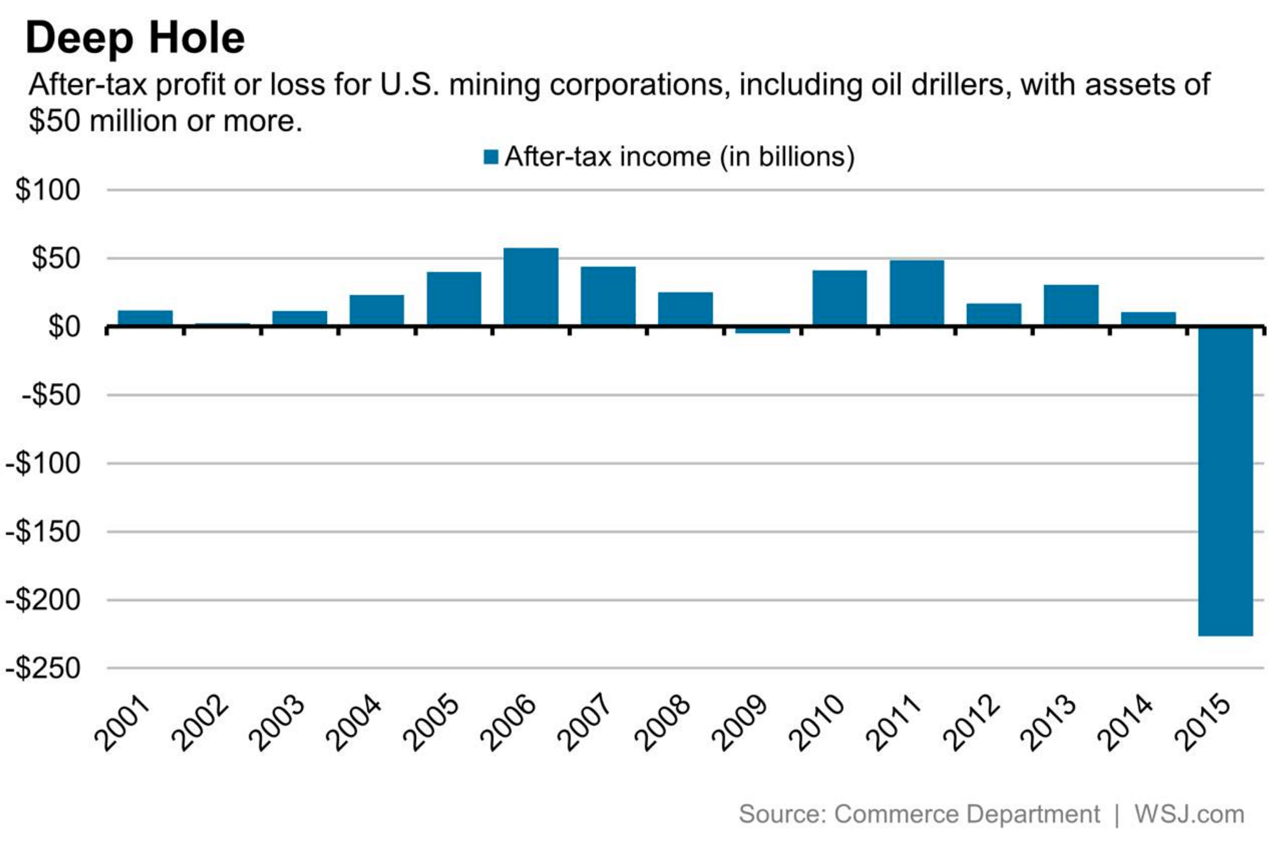

Nobody would deny that the oil sector has had it tough recently. And this week’s graph shows us just how tough it’s been.

The graph is simple, the message clear. What it shows is what the development of total earnings for the mining sector in the US over the last 15 years has managed to generate annually. Although the mining sector includes more than oil exploration, it’s evident that the oil sector’s share has increased significantly over the years. Relative to 2007, oil production had risen by 80% by the year 2014, a percentage that would probably have risen to as much as 100%, had it not been for the fact that the success of the shale revolution has not left the price of a barrel of oil unaffected. As we know, oil prices plummeted from over 100 dollars a barrel to a low of just 25 dollars, reached earlier this year.

While it was still lucrative to extract oil from the ground at 100 dollars, once it had broken below the 60-dollar mark, the party was well and truly over. In late 2015, the price of a barrel of oil was 40 dollars, with losses being suffered as a result. Huge losses, as the graph makes clear. The mining sector reported cumulative losses of 227 billion dollars for the year 2015. These losses are as big as all the profits in the previous eight years added together. To put that into a bit more perspective: that is roughly a quarter of the size of the economy of the Netherlands. It’s not as big as the amounts we saw during the banking crisis in 2008, but it’s impressive enough.

Black swan

I find this graph so interesting because it is, in my eyes, a perfect example of a Black Swan event. The term Black Swan is the title of a book by Nassim Taleb, who popularized the concept. It relates to events that are rare, unexpected and also with a major impact – on the global economy, for instance. Or, as he states himself on Wikipedia:

What we call here a Black Swan (and capitalize it) is an event with the following three attributes.

First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility. Second, it carries an extreme ‘impact’. Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.

I stop and summarize the triplet: rarity, extreme ‘impact’, and retrospective (though not prospective) predictability. A small number of Black Swans explains almost everything in our world, from the success of ideas and religions, to the dynamics of historical events, to elements of our own personal lives.

No one expected in late 2013 that the price of oil would fall below 40 dollars within just two years. Sure there were some folk walking around predicting 200 dollars, but the idea that oil prices would ever return to their low of 2008, let alone drop further, was really inconceivable.

And let’s be in no doubt that this has a wider impact. Suppose you’re a bank asked to grant a loan to a company in this sector. It’s 2014 and you only have the graph above at your disposal, with the exception of the last year, obviously. I guess that you as a bank would be delighted with such a client: operating in a sector that has pretty much only generated profits. Only in 2009 – the deepest recession since the thirties – was a small loss reported, but those losses were relatively modest compared to all the other carnage we saw that year. It would seem very reasonable then, wouldn’t it, to grant a loan to such a client?

And then a Black Swan came drifting by …

It’s easy to see why the US stock market was gripped by these oil-price developments at a certain point: with such a massive, unforeseen event, the chips can fall in the most unexpected ways. In that sense, the damage up to this point doesn’t really seem to be that bad, as suggested by the graph below from Bank of America. This graph shows default rates for companies with outstanding bonds, divided into sectors. So the real pain really does seem to be mainly concentrated in the most logical sectors: energy, commodities and capital goods.