https://www.bespokepremium.com/think-big-blog/oil-and-equities-correlation/

If you wanted to comment sagely on equities over the last month, all you had to do was to check out the development of oil prices. Is that normal or is it an aberration?

If you’d been following market developments since the beginning of the year, you can’t have failed to notice the dominant role played by oil. Each decline in a barrel of crude translated almost directly into a drop in equity prices, leading stock market experts to turn overnight into oil experts so they could comment sagely on short-term market developments. The strength of this connection is perfectly illustrated in the graph below, which shows the link between European equity market levels and oil price developments over the first month of the year. I’m specifically looking at intraday moves here, so not just opening and closing positions.

You could also convert the graph above into a scatter diagram, with each observation shown as a combination of the level of the equity market and the price of a barrel of crude oil. This gives us the following picture, with oil on the vertical axis and European equities on the horizontal axis.

The link is of course not perfect – not all observations fall precisely on the black line – but based on my experience I can say that this is an improbably high correlation for financial markets. Based on this link, you can calculate that a decline in oil prices of 1 dollar per barrel in this period correlates roughly with a 1% drop in European markets. By the way, I use the word ‘correlate’ advisedly, of which more later.

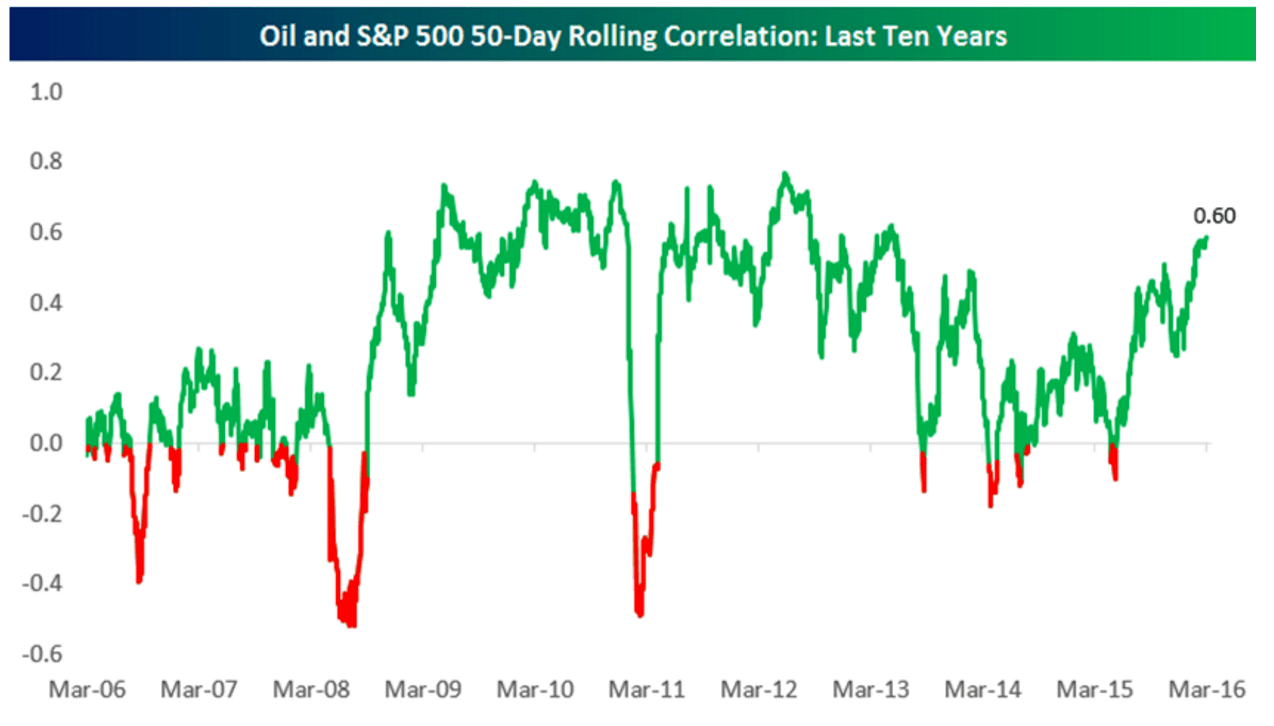

Normal or an aberration?

That brings me back to the question: is this normal or an aberration? The striking conclusion of the graph this week is that it is more often normal than an aberration. What the graph shows is the correlation between the price development of a barrel of crude oil and that of the S&P500. Specifically, we’re looking here at the daily percentage change in both variables, showing how high the correlation was over a period of 50 days. By shifting the period of 50 days forward by a day at a time, we get an idea of how the correlation has developed over time.

So? Well, it turns out that the correlation has gradually increased over the last few months, but the current correlation of 0.6 is not unusual. What’s more, in 2010 and 2012, the correlation was fairly consistently higher, peaking a high as 0.75. Actually, what we’re seeing now corresponds with developments over those years: nothing new under the sun, then …

Now, there is no arguing with simple mathematics – I’ve checked the graph and it’s correct – the outcome doesn’t align at all with my perception of what the world looked like five years ago. Nobody was lying awake in 2010 worrying about what was happening on oil markets. Euro crisis, yes. Fed monetary policy, absolutely. But oil? Oil was simply not a dominant factor in that period – there weren’t any traders nervously watching oil price developments morning, noon and night. However, things were very different over the last few months.

This is a typical case where simple statistics fail to show the underlying changes in fundamentals. In 2010, we were in a recovery period following the recession of 2008–2009. Equities were bouncing back, the economy was improving, and commodity markets were making good previous losses. The stock market and oil were not so much reacting to each other, but rather to signs of economic recovery and an increase in confidence about the future. And in 2012, too, we were witnessing an upturn in optimism that led to a synchronous movement in both markets, rather than one market driving the other. This is a typical example of where both markets are responding to a third factor and not to each other. Or, in statistical terms: correlation does not automatically imply causation. A classic example to illustrate this is to consider visits to the swimming pool and ice cream sales. Both show a strong increase on the same days, but this does not mean that ice cream sales result in more visits to the swimming pool. Obviously, it’s warm summer weather that causes both.

But what we’ve seen in recent months is that equity markets have been very specifically reacting to developments in the oil market. Naturally, the underlying economy (and sentiment) are also playing a role, but the fact is that every trader in the world is keeping a very close eye the price of oil is something we definitely didn’t witness in 2010–2012. The decline in oil prices had a direct impact on equity markets via a number of channels. Not only was increased credit risk having a direct impact on the market (fears that oil companies and/or maybe even banks would go bankrupt), but also declining oil prices were leading to the liquidation of some of the investment portfolios of oil producing countries, which equally led to price declines. So it was logical that we were watching the oil market. Logical, yes, but not usual or normal.

Another way of answering the question as to whether the current situation is ‘normal’ or rather slightly unusual, is to trace the first graph back a bit further. That gives us the following picture:

It turns out that in the period 1990-2008, the correlation almost never exceeded 0.4, and even if it got that far, it didn’t stay there for long. Periods of high correlation followed periods of negative correlation in quick succession. What’s more, on average, the correlation over this period was even as low as -0.05, which suggests that oil and equities didn’t show any structural correlation.

Although the graph seems to indicate that what we are now witnessing is nothing special, I’ve still got a strong feeling that the current preoccupation with the price of a barrel of oil is unique. And that means the link is more likely to be temporary than permanent.