http://uk.businessinsider.com/bank-of-america-seven-year-glitch-note-2016-3

So commodity prices are under pressure, again – nothing new there, it’s hardly unusual. But what’s going on at the moment is rather more pronounced …

No one could have missed the mini-revolution that has taken place in energy markets over the last two years. The rise of the shale industry, the strong growth of solar energy and the implosion of OPEC have all resulted in oil price declines to the tune of 70% over the last 18 months. ‘Peak oil’, the fear that we have passed maximum oil production, turned out to be another wraith, with all the repercussions that implies. However, if you examine the commodities market more carefully, you’ll see that the losses are not limited to the oil sector. From copper (-35%) to coffee (-40%), from cattle (-25%) to silver (-25%), this last year has seen most commodity markets under pressure.

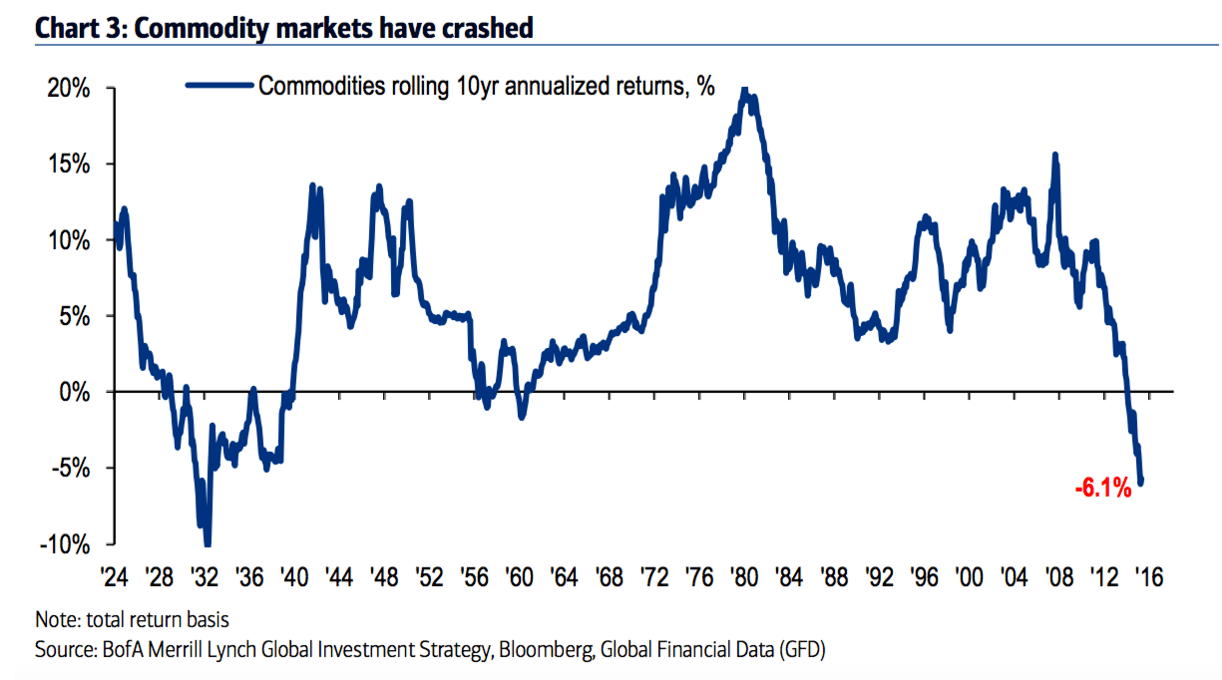

And it’s clear from today’s graph that this trend is not only limited to last year. The line shows what you as an investor would have earned if you had invested in a broad index of commodities. This does not take into account annual gains, but rather what you would have earned over the longer term – a period of ten years. The outcome: if you had invested in a broad basket of commodities ten years ago, then that would have generated an annual loss of 6.1%. To put that into greater perspective: of the 100 dollars you invested in 2006, you’ve got just 53 dollars left right now.

And if I replicate the graph myself, I see an even more desperate picture emerging. Looking at the Goldman Sachs Commodity Index, the development of total returns appears as follows (thick blue line). According to this index, the average annual return is -10.5%, which means that your original 100 dollars is now worth just 33 dollars …

How to make an index?

So what is the real number: -6% or -10%? They are probably both true, the difference being in the underlying index used. If you’re talking about ‘the’ commodity prices, you quickly run up against the problem that there are no fixed rules for adding the price development of say oil to that of say cattle. Although with equities and equity indices you can still assert that the size of a company is leading, this is not so much the case when you compare cotton with silver.

The reason the Goldman Sachs Index is so negative will become clearer if we look at the second graph, where I show not just the whole index, but also the main subcategories. So what catches your eye? The blue line (total index) correlates to a large degree with the development of the green index (energy), and less so with the purple or orange lines, for example. This is down to the fact that the Goldman Sachs Index allocates a much heavier weight to the energy market than to other commodities. The graph below shows the difference in composition between the Goldman Sachs Index (right) and that of the Dow Jones (left). Goldman Sachs focuses on the economic weight of the commodities market, but Dow Jones limits this to ensure a more balanced index. That’s a bit like how the AEX also applies rules to ensure that the weight of a single company (read RoyalDutch) does not become too dominant in the index.

http://www.indexologyblog.com/2014/07/10/weighing-in-reaching-your-goal-weight/

Regardless of the weights chosen, it’s hard to deny that what we have witnessed over the last ten years is quite exceptional. As demonstrated by the first graph, you need to go all the way back to the thirties (the Great Depression) to see such a poor return. So it’s not without reason that equity markets, for instance, have been affected in recent months by developments in the commodities market. What if the fall in commodity prices is a sign of (strongly) declining demand?

No Great Depression

Nobody can deny that the global economy has slowed somewhat, but the idea that we are in a situation comparable to the Great Depression doesn’t hold much water. As I said, there are specific reasons that drive the price development of the oil market, including not only demand but also supply factors. What’s more, commodity markets are particularly sensitive to economic developments in the world’s largest commodity ‘consumer’: China. So although it’s clear that economic growth has slowed, even when we take the bleakest estimates of real growth of 2 to 3% (different than officially reported growth), it’s quite a stretch to talk of a Depression.