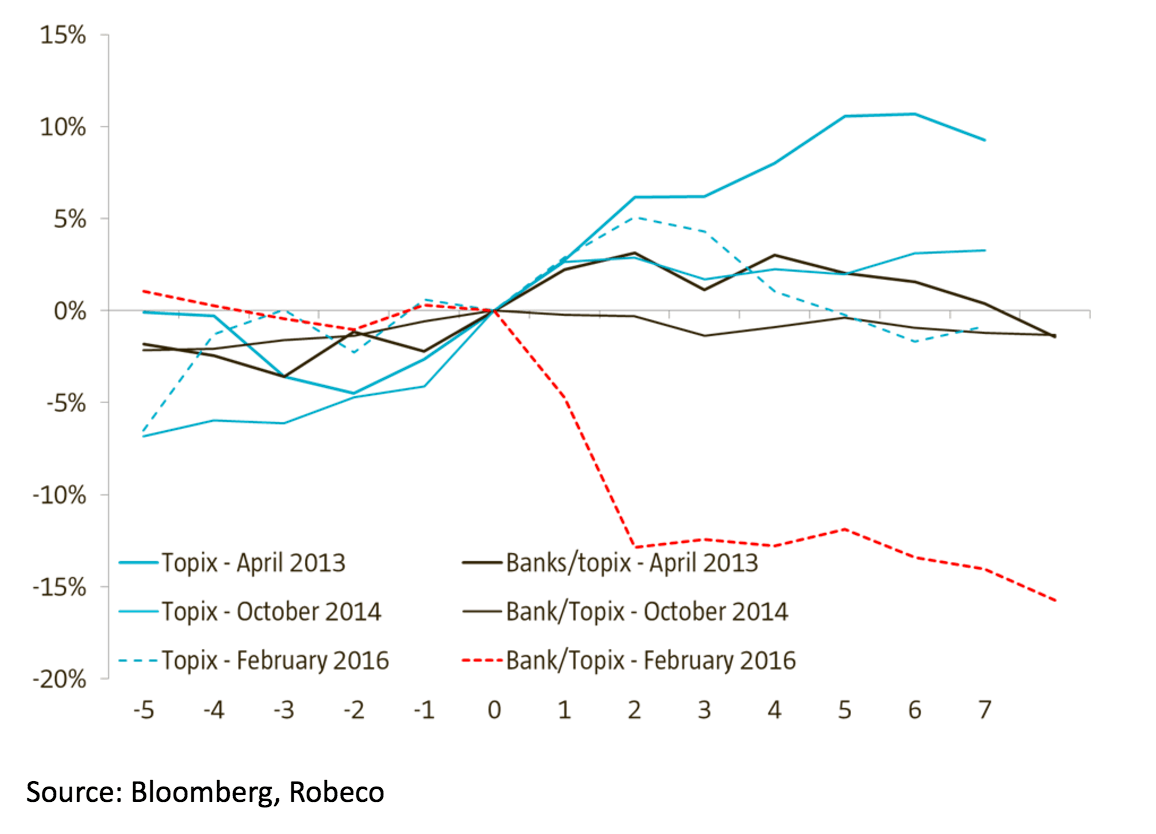

When the Japanese central bank took both friend and foe by surprise at the end of January with its introduction of negative deposit rates, this initially had the desired effect: the Japanese yen weakened and equity markets rallied. However, there was one clear signal to suggest that it would turn out very differently this time. Whereas equity markets reacted positively in general terms, a part of the market showed a very different response: the Japanese banks. With the Nikkei 5% higher just two days after the interest-rate decision, the TOPIX bank index lost 8.5% over the same period. The reason? Fears about the profitability of banks in a negative interest-rate environment. The negative deposit rates mean that from now on commercial banks have to pay interest to the central bank on their credit balance. Partly due to this development – not to mention concerns over Chinese growth, oil markets and the US recession – sentiment turned and Japanese equities subsequently plummeted 15% in two weeks that followed. If the plan of the Bank of Japan was to stimulate the Japanese banking sector to pump idle capital into the economy, then we can safely say that this was not the most effective way of doing it.

Now I’m not a bank analyst, so everything I write from this point on needs to be taken with a pinch of salt, but -8.5% because the deposit rate was lowered from 0.0% to -0.1%? Was such a small interest-rate reduction then really so disastrous for the profitability of the Japanese banking sector? This seems somewhat unlikely, especially when you realize that the -0.1% only relates to a limited portion of Japanese deposits. And if it really was that bad, you’d have thought that the Bank of Japan would be aware of it, right?

But is it as bad as that?

Enters www.alphaville.com, the somewhat geeky and technical website of the Financial Times, where this sort of question is discussed. During the last month, there have been a number of posts that looked at the fragility of the banking sector to negative interest rates. This was not specifically related to Japanese banks, but more to the experience of banks in countries in which negative interest rates have been applied for some time already: Switzerland, Denmark, Sweden. The graph below, for instance, shows the changes in the net interest income of Swiss banks. With negative interest rates, you’d expect that this part of the profitability of the banks would be under pressure. But there is absolutely no sign of earnings erosion: despite the implementation of negative deposit rates, earnings have risen almost across the board.

The next graph also suggests that the sensitivity to deposit rates is really not that bad. This graph comes from Credit Suisse and shows the performance of the banking sector for the different countries for this year so far. And it turns out that the countries with the most negative interest rates (Sweden and Denmark) show the least negative performance. Granted, the graph is now two weeks old, but at least it does not support the story that negative interest rates are really that negative for banks.

http://ftalphaville.ft.com/2016/02/24/2154137/negative-rates-havent-hit-banks-all-that-hard/

And yet, it seems strange to suggest that negative interest rates would have no effect whatsoever on the profitability of rate-dependent operations, something that is indicated in the graph of the Swiss banks. Individual savers do not yet pay negative rates, so you would have expected the lower deposit rate to have genuinely affected rate-dependent operations. According to the analysts at UBS, this is partly because the Swiss banks have ‘raised’ mortgage interest to compensate for the reduction in the profitability of savings-dependent operations. On balance, people taking out mortgages are subsidizing individual savers.

All things considered, the idea that earnings are being stripped because of negative rates seems to be somewhat overdone. On the other hand, you might wonder whether say a Swiss central bank could have expected mortgage-market rates to rise as a result of a decline in short rates…