After the success of GDP Nowcasting, we now have inflation Nowcasting. Better than consensus – what more do you want? Well, erm …

I suspect that half my readers will have left by the end of this introduction, as terms like Nowcasting and consensus will not be directly familiar to everyone. So first an explanation, beginning with Nowcasting. Nowcasting is a collective term relating to attempts to try to make some sense of economic developments based on the most recent data available. Think in terms of inflation data based on prices charged by online supermarkets, or even estimating an economic (or market) trend based on ‘the mood’ on twitter or Facebook (more smileys is good for the economy!). The whole idea is that you get a must faster (and hopefully more accurate) picture of the state of the economy and that you don’t have to wait a month or a quarter for the official figures to be published.

Not all initiatives are equally successful, but one that has built up a very solid track record over the last 18 months is GDP Nowcasting by the Federal Reserve Bank of Atlanta. This indicator doesn’t focus so much on information from the internet or likes on Facebook, but limits itself to the official data published weekly or monthly. Initial jobless claims, producer confidence and consumer prices all form the basis of this index and the results are not to be sneezed at. See (https://www.frbatlanta.org/-/media/Documents/research/publications/wp/2014/wp1407.pdf?la=en) for a full explanation of the methodology used.

It’s interesting that the GDP Nowcast is currently predicting a growth percentage of 2.6% for the first quarter, which is clearly above consensus expectations of 2.1%. ‘The’ consensus is in this case the average estimates of ten analysts considered reliable by the Atlanta Fed. In actuality, there are many more analysts that provide estimates, so the definition of consensus here is not exactly set in stone. On Bloomberg I see no less than 68 analysts of reputable banks who have published estimates for the first quarter. But they too have an average of around 2.1%.

https://www.frbatlanta.org/cqer/research/gdpnow.aspx?panel=2

For clarity’s sake: the consensus number is a prediction, and Nowcast is the best estimate based on the information published up to that point. Nowcast may yet converge down towards consensus, if data over the coming weeks come in weaker. So the real difference in quality between Nowcast and consensus can only be determined on the day the GDP figures are published. Until now, Nowcast has indeed proven itself in the end to be more accurate than consensus. Given that the consensus is made up of analysts who are also aware of Nowcast, we now see a trend whereby the consensus starts to converge with the Atlanta Fed’s estimate in the last few days before publication. In short: Nowcasting is gradually taking over the role of consensus.

So now to inflation

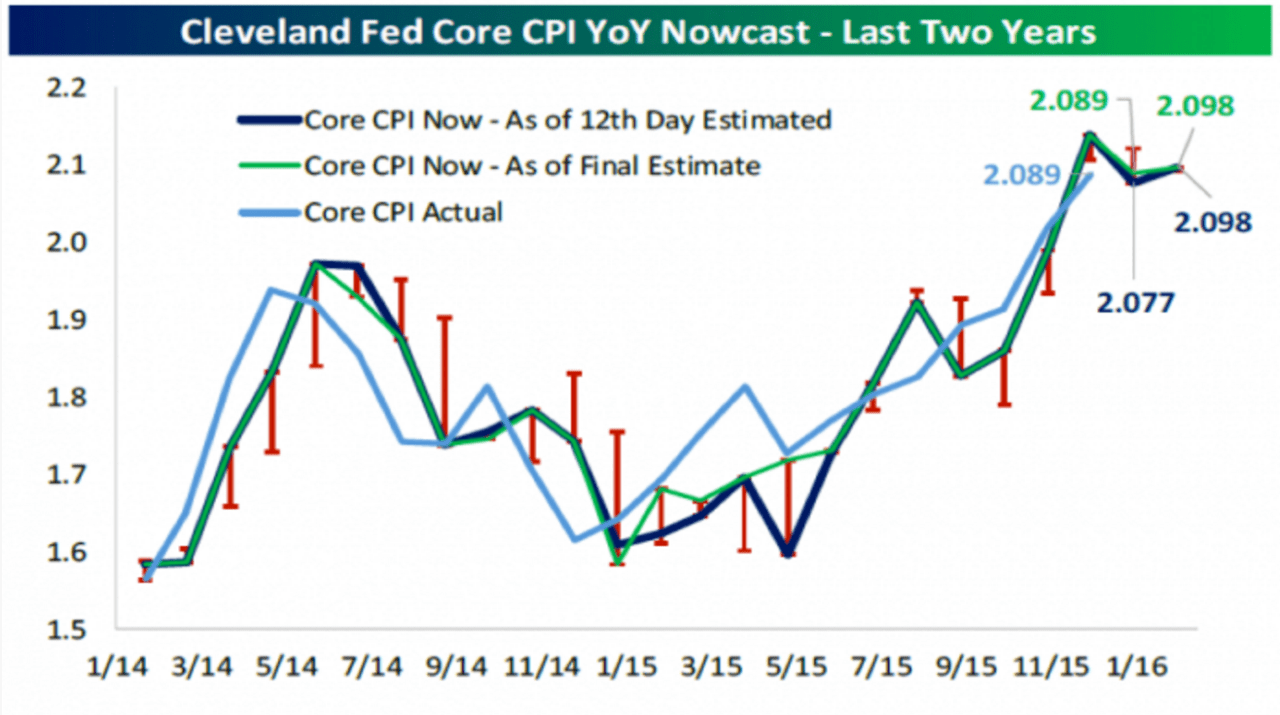

The Cleveland Fed must have thought, if the Atlanta Fed can do it, so can we. But creating a second GDP Nowcaster would have proved a little tedious, so they came up with the idea of constructing an inflation Nowcaster. So you can now check out daily the best estimate for inflation over the coming month, taking account of gas prices and weekly retail trade numbers. The good news is that this estimate also turns out to be more accurate than estimates produced by the consensus the day before publication of the numbers concerned. At least that’s the conclusion of the Cleveland Fed itself in its accompanying study. (https://www.clevelandfed.org/~/media/content/newsroom%20and%20events/publications/working%20papers/2014/wp%201403%20nowcasting%20us%20headline%20and%20core%20inflation%20pdf.pdf?la=en)

And yet, I’m not sure this will become as big a success as the GDP Nowcast. The big difference between GDP and inflation is that the former is only published once every quarter, while the latter comes out monthly (several times a month, actually, if you consider that in addition to the official consumer price index (CPI) we also have the deflator of consumer spending (PCE), the producer price index (PPI), and the wholesale price index (WPI).) There seems to be more than enough news on inflation, so a regular update appears to be somewhat unnecessary. What’s more, the composition of the GDP figure is much more complex and multidimensional than that of inflation, so the inflation Nowcast is a lot more straightforward.

What’s more, if I take a look at the graph above, I get a strong sense that the Nowcast estimate lags the trend in real inflation by a month. In other words, the light-blue line (the number that Nowcast tries to estimate) started to decline in 2014, and to rise in 2015, one month (or two) earlier than the estimate from Nowcast itself (green and dark-blue). You sort of hope that the estimate actually precedes the real figure and not the reverse.

And let’s be honest here: when was the last time that markets reacted surprised based on an unexpected inflation figure? It is undoubtedly important to the underlying trend in the economy, but it’s usually a bit of a non-issue on financial markets. And, yes, I know it’s not just about financial markets, but the success of this indicator partly depends on the popularity of the underlying data series. So if I may be so bold as to give the guys at Cleveland a tip: create a Nowcast of the monthly payroll report. If you succeed in turning that into a superior indicator, then the first Friday of each month will be a whole lot quieter!

Pingback: A strong quarter! | Best of the Web

Pingback: Bond yields and growth | Best of the Web

Pingback: Good news for Trump! | Best of the Web