http://uk.businessinsider.com/closing-bell-february-1-2016-2

For the fourth consecutive month US producer confidence is below the neutral ‘50’ level. What should we make of this?

Let me start by correcting myself: there is no such thing as the ‘US producer confidence’. What does exist, is a deluge of data giving an indication of producer confidence in parts of the US economy, some of which relate to regions (Philadelphia, Chicago) while other parts relate to sectors (industry versus services). This may seem like an irrelevant detail – but it’s far from that. If we look at the two main national confidence indicators, we currently see significant differences. Producer confidence in the industrial sector is in negative territory (<50) for the fourth consecutive month now, while service sector confidence is still safely above the neutral level (53.5). When you then consider that the US industrial sector accounts for around 16% of GDP, while the services sector is more than four times the size, it’s easy to see why this isn’t just an irrelevant detail.

This may cause you to wonder why we still see graphs based on the ISM Manufacturing Index so often. The answer is simple: the ISM Manufacturing Index has been produced since 1948, while the Non-manufacturing Index only since 1997. So, the sample for the ISM Manufacturing Index is much bigger. In addition, you could say that the direct weight of the industrial sector is not particularly significant, but the indirect effect probably is: suppliers, financial services, maintenance are all related to industrial activity, but often defined as services.

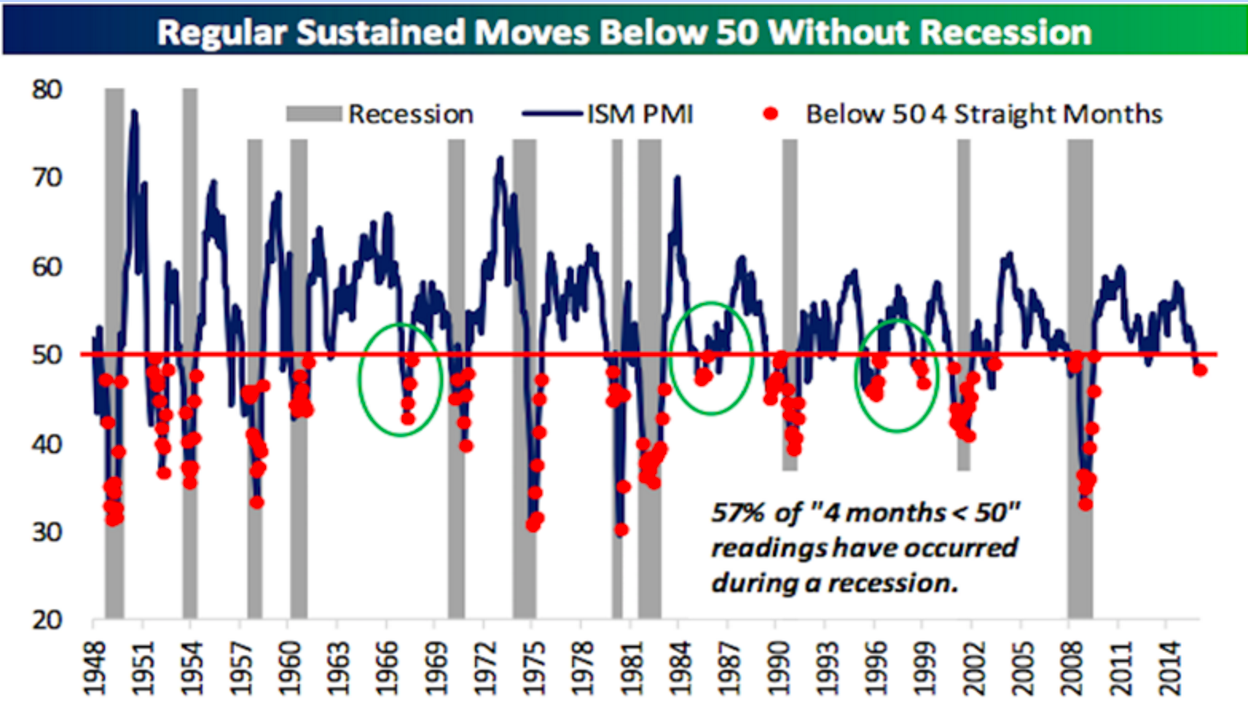

Finally, I get to that graph

With that introduction I finally get to the graph. What it shows are the movements in the ISM Manufacturing Index since 1948 (blue line), US recessions (gray bars) and the number of times the ISM Manufacturing Index has been in negative territory for at least four consecutive months(red dots). The makers of this graph have then counted all the dots and concluded that 57% of them occur in a period of recession, and 43% don’t. In short: four consecutive months of producer confidence below 50 is quite a risky scenario.

Does it keep me awake at night? Not really. What strikes me first is that the link seems to have weakened over the period covered by the graph: while in the first half the red dots almost always correspond with recessions, this has happened less frequently since 1980. On the face of it, this ties in with the fact that the importance of the industrial sector has slowly but surely diminished during this period. As I have said in the past, the fate of the US economy is less related to what is happening in the industrial sector and more to what is happening in the services sector. The graph also clearly shows that the current fall in producer confidence in the industrial sector is not yet that spectacular; it’s mainly the oil-producing sector that’s feeling the pain, while the narrower measure of the manufacturing sector has yet to show any contraction. Counting the number of sub 50 months is far less telling than the maximum gap. That gap is currently not very substantial.

Better graph

Initially I thought the graph showed something different: for a moment I thought the black line depicted the movements of the S&P 500, which would then show you the link between the stock market and the industrial sector. But it doesn’t. So I made this graph myself – showing the price movements of the S&P 500 from the point when the ISM Manufacturing Index falls below 50 and remains there for four consecutive months (as is now the case). In doing so I looked specifically at the S&P 500’s lows, not its month-end levels. Your maximum loss, so to speak. The gray bars represent recession periods here, too.

What does it show? Periods in which the ISM falls below 50 that don’t culminate in a recession result in maximum losses of 15% (1998), but the loss is only temporary. In most cases you see that the market soon recovers and even ends higher by the time the ISM Manufacturing Index rebounds above the 50 again

So basically, as long as we can avoid a recession, the market will be fine too. Or, at least, it will if past events dictate what will happen in the future…