http://www.marketwatch.com/story/a-bear-market-in-stocks-became-more-likely-today-2016-01-04

When markets closed heavily in the red on the first day of trading in the new year, all sorts of statements were made about how this year’s fate had been sealed. And since then the losses have only got worse: bad omen or not?

Question: when was the last time markets lost 7% in one week? Late August. And before that? December 2014. I suspect most readers can still remember the August correction, but December 2014? And yet, it’s true: from close on 8 December to close on the 15 December 2014 the Amsterdam exchange lost 7.3%. A painful slap that must have caused a lot of turmoil in that time, but that we can barely remember now. Dustbin of history. Because this happened at the end of a pretty strong year, the fate of that single down week was sealed in advance.

And that’s the difference between the first trading day or week of the year and all other days or weeks. Throughout the year, the closing level of the AEX on 31 December is seen as the benchmark for the new year, so a poor first week sticks in the memory for much longer than a bad week some other time during the year. And that applies much more so to the first trading day: closing 4 January with a loss of 2.3% somehow feels more threatening than the 3.7% loss on 3 December 2015. What’s more, in 2015 there were 12 trading days with larger losses and I’ll bet that there are few people who could name them.

The conclusion? It’s important to emphasize that we seem to place greater weight on the first trading day and the first trading week of a year.

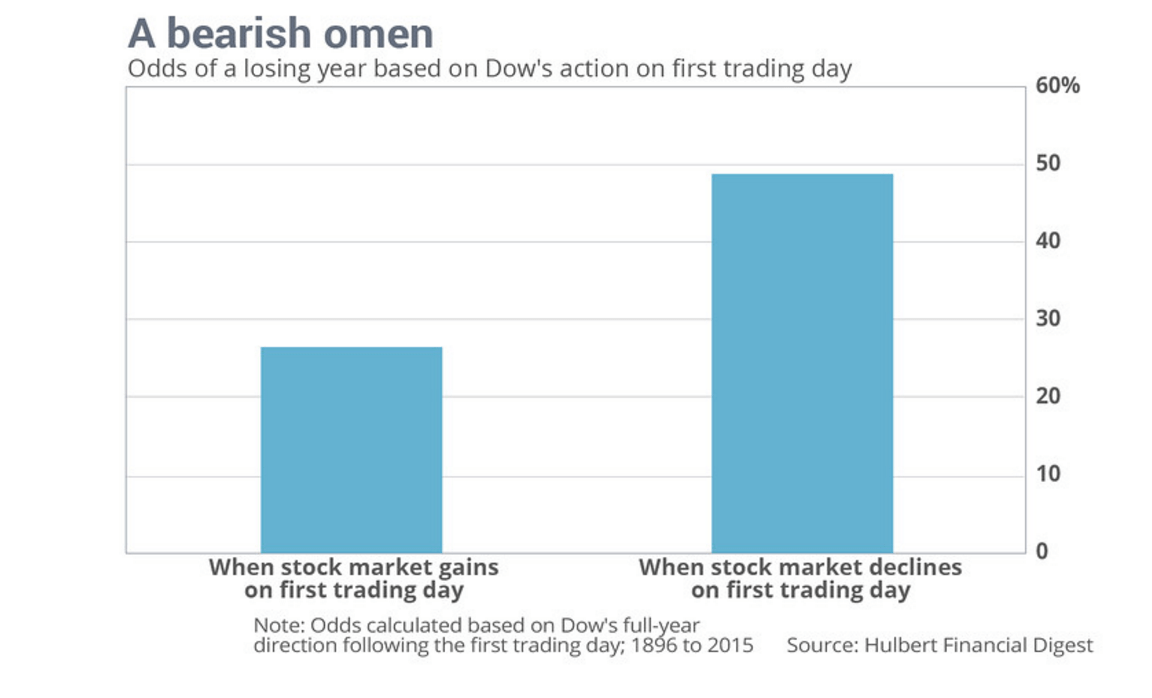

Which finally brings me to this week’s graph. It’s a very simple thing that shows how often the market (the Dow Jones in this case) closes the year with a negative result. The left-hand column shows the percentage for years in which the first trading day was positive, and the right-hand column the percentage for years in which the first trading day was negative. In words: after a positive first trading day (left hand side), the chance of a negative trading year is 26%, but after a negative first trading day (right hand side) that percentage rises to nearly 50%. As a nerdy statement: above the graph it states incorrectly that these are ‘the odds’. They are not: these are simply the results we have observed in the past, but that’s a minor quibble.

I must say it looks very impressive. But one note of caution to state from the off is that we still have 50% odds on a positive close to the year after a negative first trading day, so we can conclude straight away that it’s too early to write off 2016 just yet.

True relationship or statistical noise?

However, the question is whether this is a genuine relationship or just statistical noise? What do things look like, for instance, if we take the second trading day, the fifth or the twentieth? Based on the data, I had a go at working out whether the first trading day really is so important. I used data from the S&P500 going back to 1928, which could lead to some differences, compared to the previous chart

First let’s look at the distribution of the probability of a negative year after a first positive trading day. This means looking at the result that you would have realized one year after the trading day in question. For example: if the 153rd trading day was positive (somewhere at the beginning of August), how often did the 12 subsequent months have a negative return? That’s basically the left-hand column in the first chart, but then across the entire year.

It turns out that the 26% basically is neatly in the center of the distribution. In other words, after a positive trading day the odds on a positive trading year are relatively high. Historically, the 71st trading day of the year is the best ‘predictor’: in only 14% of cases did a negative annual return follow a positive trading day.

The second column (the percentage of stocks closing lower after a negative trading day) looks as follows when spread across the year:

What jumps out straight away is that I don’t reach the 50% for the first trading day of January. This might of course be because I’m using the S&P, but it could also be down to the negative connection being stronger in the years prior to 1928. Strikingly, in my graph the first trading day is slightly above average, but once again does not show the biggest deviation – the 19th trading day is much more convincing …

Should we wait?

Should we therefore wait for the 71st and the 19th trading days to determine what the best positioning should be? Better still, should we wait for the 56th trading day, as that day gives the maximum difference between the two columns in historical terms? Of course not! It is nonsense to try and say something sensible based on just one trading day, whether it’s the first or the last day of the year. This analysis conflates a -0.1% trading day with a trading day of -5%, and that naturally creates a great deal of noise. And the same applies to the result: a -2% year weighs as much as a -50% year, and that really isn’t much help.

In short: nice graph, but it won’t be keeping me awake at night. To reassure you further, another graph showing the results obtained in the past after a trading day of more than -1%. As you can see, anything’s possible.