http://uk.businessinsider.com/jp-morgan-76-chance-recession-probability-2015-12

“In this world nothing can be said to be certain, except death and taxes.” Benjamin Franklin probably lacked space, or he would have added another certainty: the next US recession.

And while we’re talking about certainties, then another is that economies enter a recession every so often. Looking back on economic developments over the last 165 years, we see that there have been 34 recessions in the US, which means on average you can expect one every five years. But that number is largely meaningless, as the frequency since WWII has been somewhat lower. So it’s pointless to suggest that recession is on its way because the last one finished seven years ago.

But you always get recession deniers. The classic example is Gordon Brown, who in 1997 promised that the era of boom and bust was over: a claim he had to retract ten years later with much reluctance. So despite all our alleged progress in understanding the economic system, we are obviously still unable to get a grip on the economic cycle. If you want to watch an excellent documentary in this subject, then the film Boom Bust Boom by Theo Kocken is a must-see.

But … when?

So there can be little doubt that the next recession is on its way, but the really interesting question is basically when. Scanning the blogosphere, it seems the chance of the next recession starting soon has increased considerably. The fall of the ISM Manufacturing Index clearly below 50, the widening of spreads in the US credit market, the strong decline of corporate earnings: dark clouds are gathering.

This week’s Graph of the Week also focuses on the risk of recession. It’s from Morgan Stanley, the bank that developed a model to provide a somewhat serious answer to the question as to when the recession will be upon us. The good news: the probability of a recession in 2016 is less than 25%. The bad news: the probability of a recession in the coming three years is more than 75% … So, brace yourselves guys!

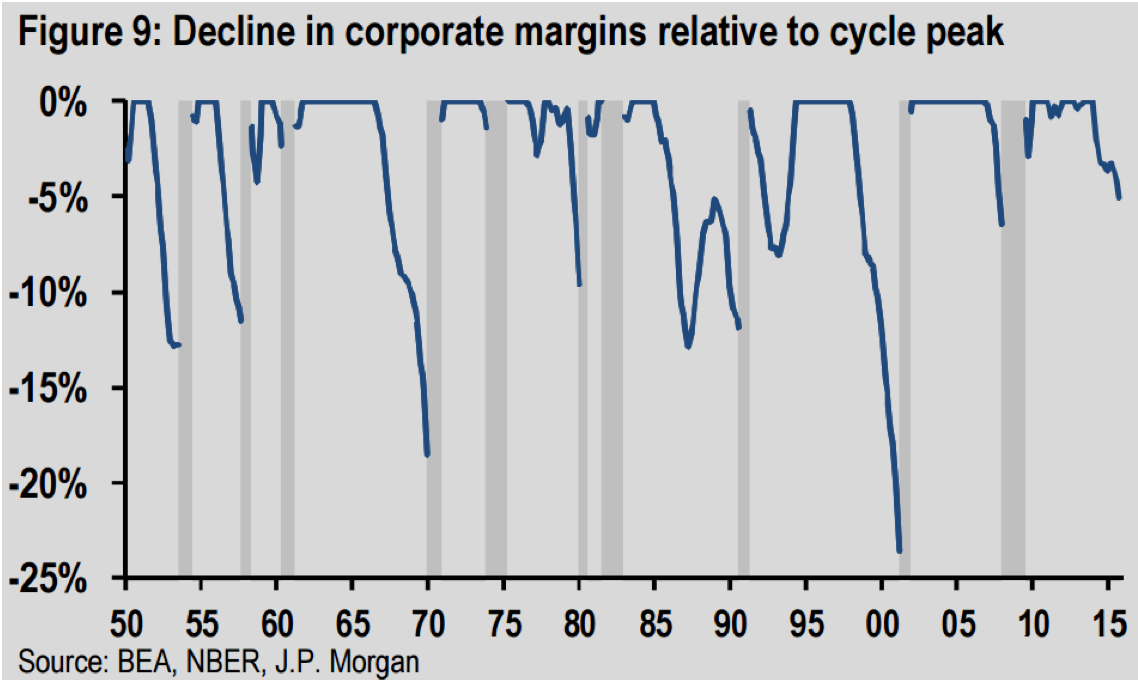

But let’s finally turn to the graph. According to the explanatory text, the above 75% corresponds to a large degree with the decline in profit margins in the US. What the graph shows is the development of profit margins during the period of expansion, with the gray areas representing periods of recession. Profit margins at the end of a recession are then used as a new starting point. If profit margins rise, then you see a straight line (the baseline is raised), and if margins decline, the line falls.

So? In the years before a recession, profit margins always decline. In all ten recessions since 1950, you can clearly see that profit margins declined, only to land in a recession. Take particular note of the decline in profit margins we have seen over the last year …

Convinced?

Am I convinced? Well, no, not really. The first problem is that there are many different indicators of profit margins, so I have not been able to perfectly replicate the graph in hand. The one that came closest is the following:

It looks similar, but it is also clear that the series isn’t entirely correct – the results don’t work either. Importantly, during my search for the correct profit margins indicator, I also found earnings figures that are showing almost no decline in margins for the current period. And that begs the question as to how strong that 75% probability depends on the series selected. But that’s not the only problem, by a long way.

What clearly strikes me, viewing the first graph, is that there are quite a few periods in which profit margins decline without this leading directly to a recession. In the sixties (four years), the eighties (six years) and the late nineties (three and a half years) recession was a long time coming. In my view, the picture changes too when you look back at the original data and not the adjusted version. The data looks like this, if I’m correct:

Looking at the graph in this way, you actually don’t see a clear pattern at all in terms of margins and recessions. In 1973, the recession fell out of a clear blue sky (margins were gradually rising). And in the recession preceding the first recession of the eighties, the margin indicator gave a false signal for two and a half years. And those aren’t the only examples. The looming decline in margins that we are currently facing suddenly looks a whole lot less threatening too: it’s the smallish peak in 2012 that makes the first graph appear to show that profit margins are declining. The last graph shows more of a sideways trend.

At the very least, it suggests that profit margin levels have little to tell about recessions. But that then begs the question as to if and why a change would cause that. Simply put, we can say that a recession is not caused by a movement in profit margins: a factor that influences profit margins may also lead to a recession, but that’s a different matter. Partly for that reason, profit margins give false signals with some regularity.

What’s more, the important thing – and something I’ve mentioned here before – is that, as far as US businesses are concerned, margin pressure can be traced to a significant degree back to developments in the oil-processing industry. I won’t deny that this sector is struggling, but the question is whether the oil sector is important enough to drive the entire US economy into recession. And based on the latest consumption figures, solid jobs growth and continuing high producer confidence levels in the services sector, the answer seems to be an emphatic ‘no’.

Whether that answer will apply for the coming three years, though, is another story altogether …